.png?width=500&name=2019%20e%20news%20spotlight%20logo%20(1).png)

Our annual rebate analysis webinar remains one of our most popular events. For 2024, we reviewed LED rebate changes by state, program, and product category, as well as trends we’re seeing in HVAC, Networked Lighting Controls, LED horticultural lighting, and EVs. Weren’t able to make this year’s webinar? Keep reading for a summary of this year’s analysis! (You can also view a recording of the webinar here. Recording will open in a new window.)

LED Program Changes

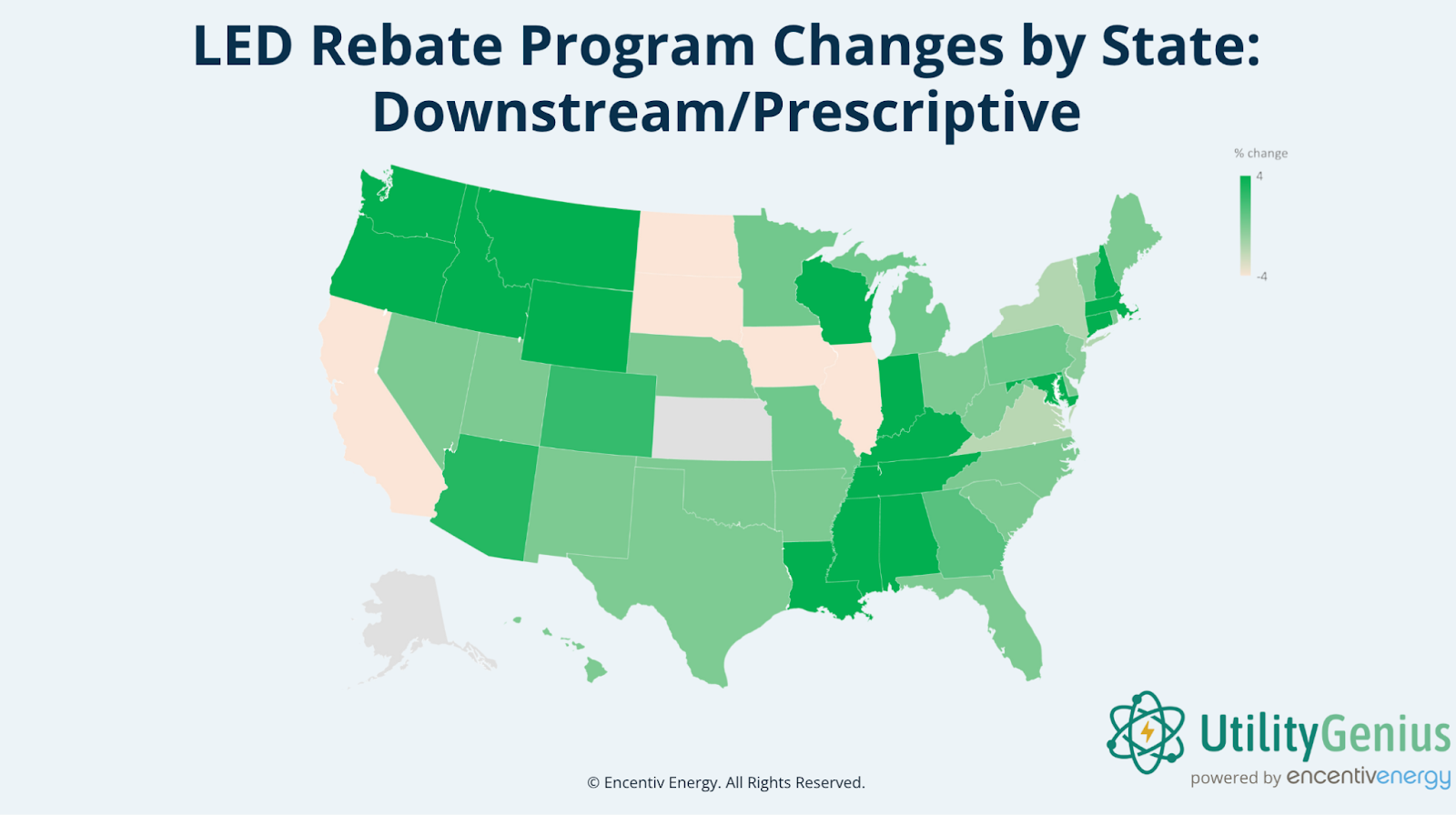

Downstream/Prescriptive

Map showing downstream LED rebate program changes by state, on a scale of +4 to -4%.

Downstream, or prescriptive, rebates are applied for and received by the end customer after purchasing eligible equipment. These involve an application process that the end user must complete, which might include pre-approval and/or post-inspection, depending on the program. These rebates have traditionally been the most common way for utilities to distribute rebate dollars.

We’re seeing a positive trend in downstream programs across North America in 2024. Net changes range from +67% to -33%, indicating that program increases have been stronger overall. In the graph above, changes have been normalized from +4 to -4%, with darker greens indicating a more positive percent change and those shown in yellow a negative percent change. Out of 51 total downstream lighting programs, 26 have increased their rates so far, with only 9 decreasing them. This capitalizes on growth seen in 2023, with programs continuing to invest in their downstream lighting rebates.

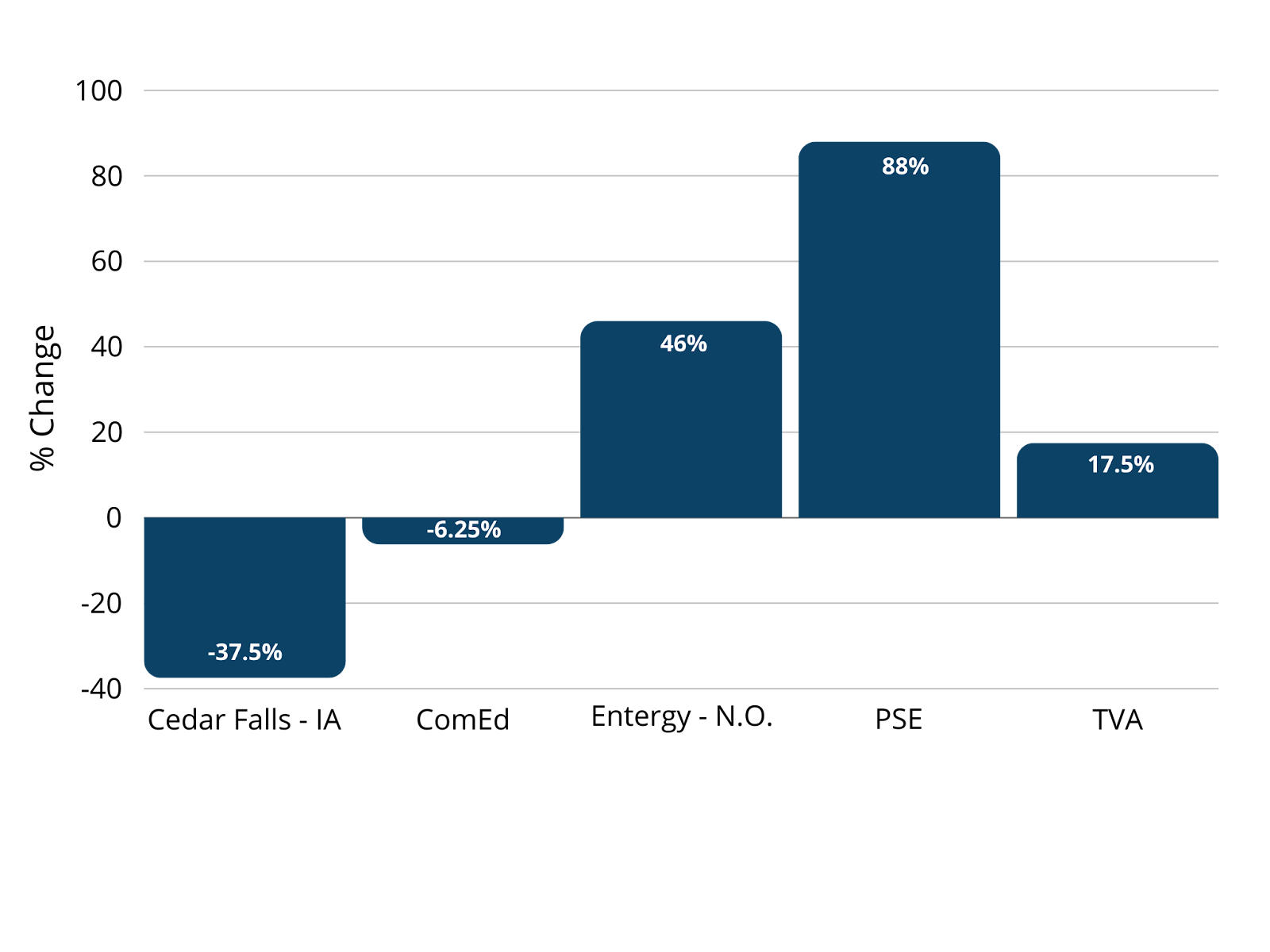

Individual program changes, from left to right: Cedar Falls (IA), ComEd, Entergy N.O., Puget Sound Energy (PSE), TVA

To break down some notable individual programs, we’ve pulled five that have caught our attention this year. Cedar Falls and ComEd both have decreased their prescriptive rates, though Cedar Falls has a much greater percent change.

On the flip side, we’re seeing some huge increases in programs like Entergy New Orleans, Puget Sound Energy (PSE), and TVA. PSE had the greater overall change at +88%, with some fixtures increasing a full 100%. TVA’s overall percent change is lower at +17.5%, but indoor lighting in the program has increased by +25%. Entergy N.O. falls in the middle, with the largest increases coming from an increase in fixture rates.

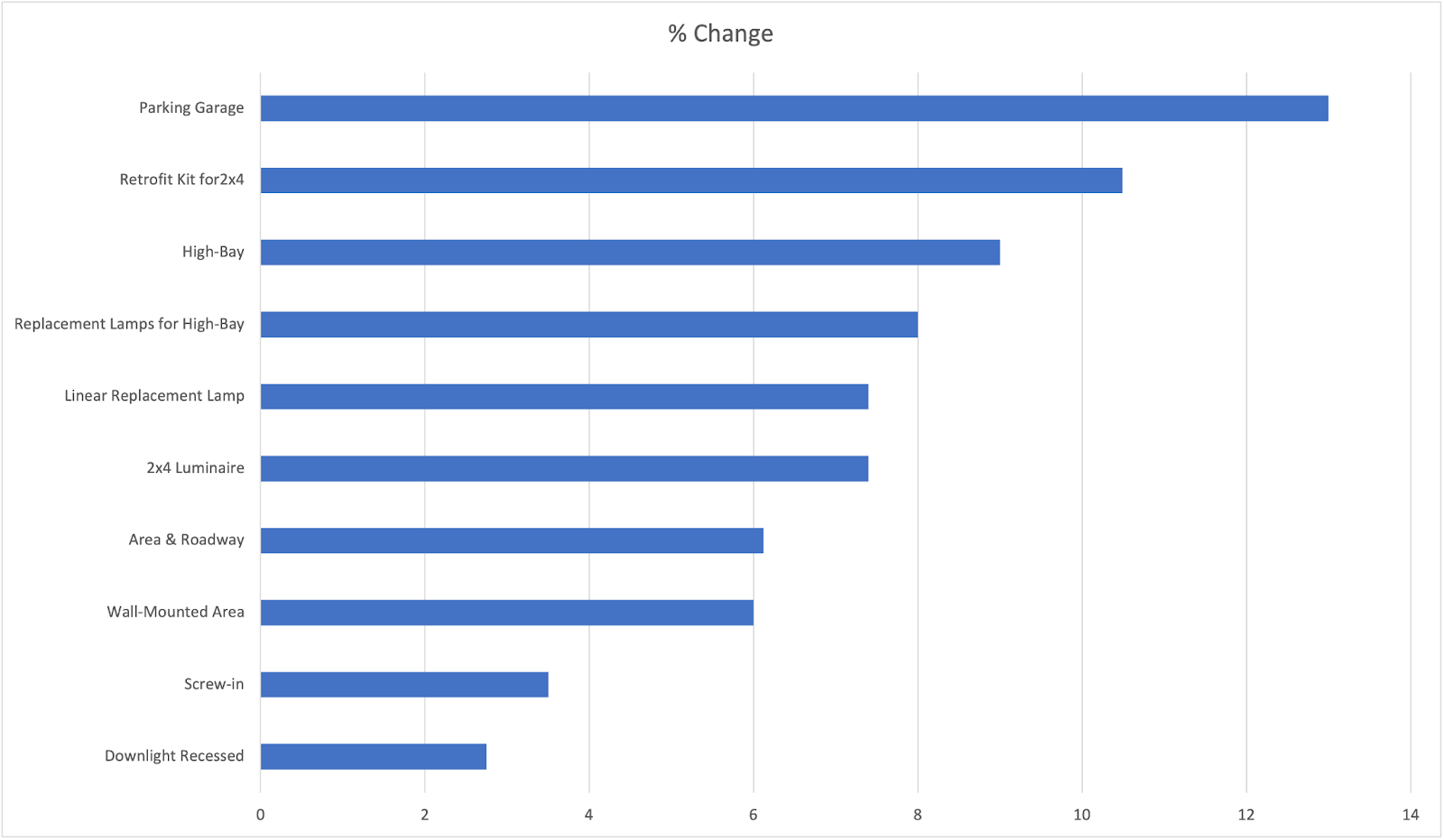

Downstream program percent changes by product category.

At the product level, we’re seeing increases in a variety of categories, with particular emphasis on fixtures across downstream programs. Despite EISA’s potential impacts on screw-ins, they saw a modest increase across programs this year, as well.

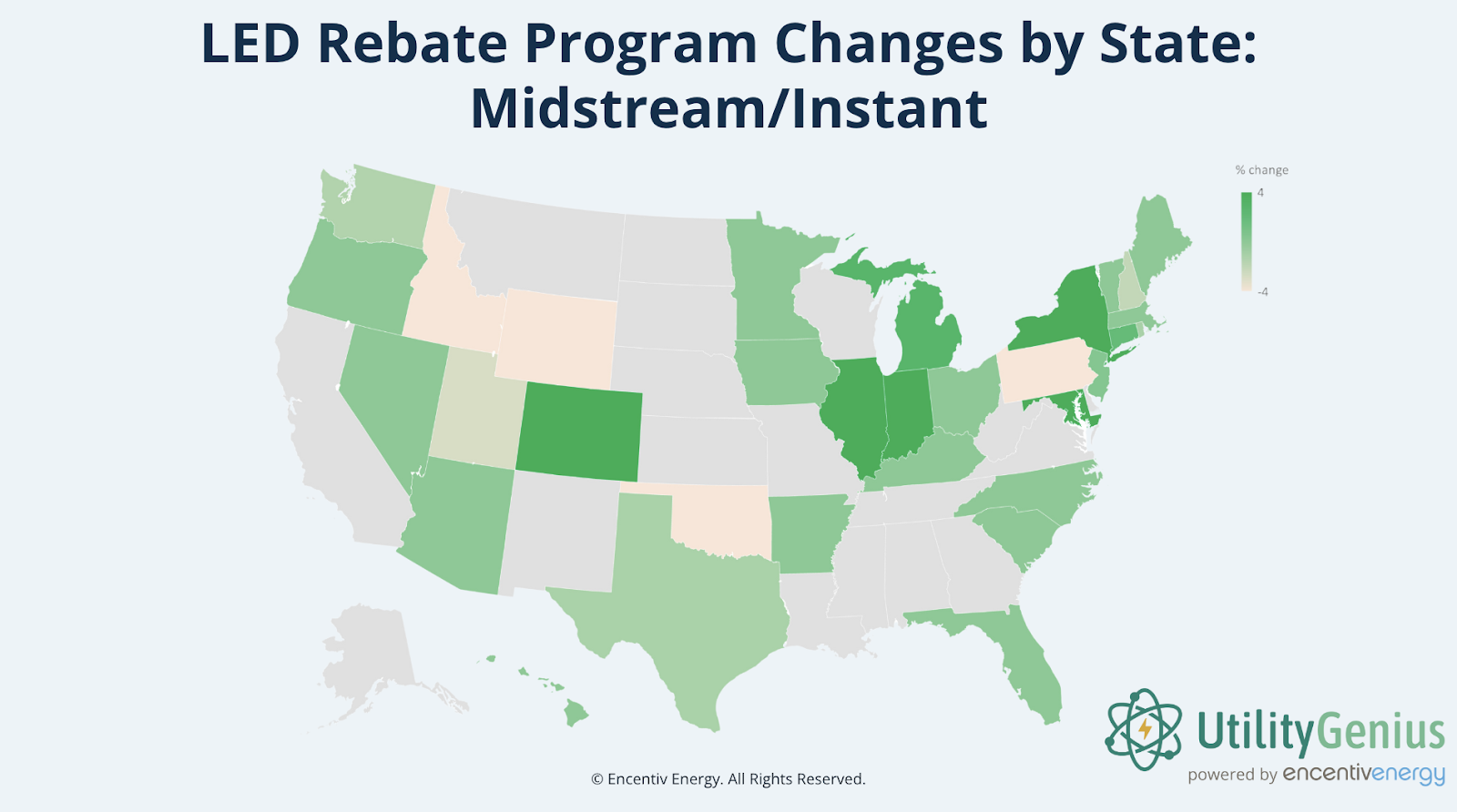

Midstream/Instant

Map showing midstream LED rebate program changes by state, on a scale of +4 to -4%.

Midstream, or instant, rebates are paid out at the distributor level, with savings typically passed onto contractors and/or end users at the point of purchase. These can be accessed through a physical retail experience or ecommerce options through the distributor. Because of how much easier they are to take advantage of, midstream rebates have been increasing in popularity over the last few years.

The above graph, similar to the downstream version, shows programs from +4% to -4%, with greens representing positive percent changes and yellows representing negative. States shown in gray do not currently have active midstream programs. Midstream programs are overall trending more positively. In fact, several major programs are going midstream only this year, including Mid-American in Illinois and Iowa, Alliant in Iowa, and IESO Save on Energy in Ontario, with New York’s ConEd slated to join the ranks at the end of 2024.

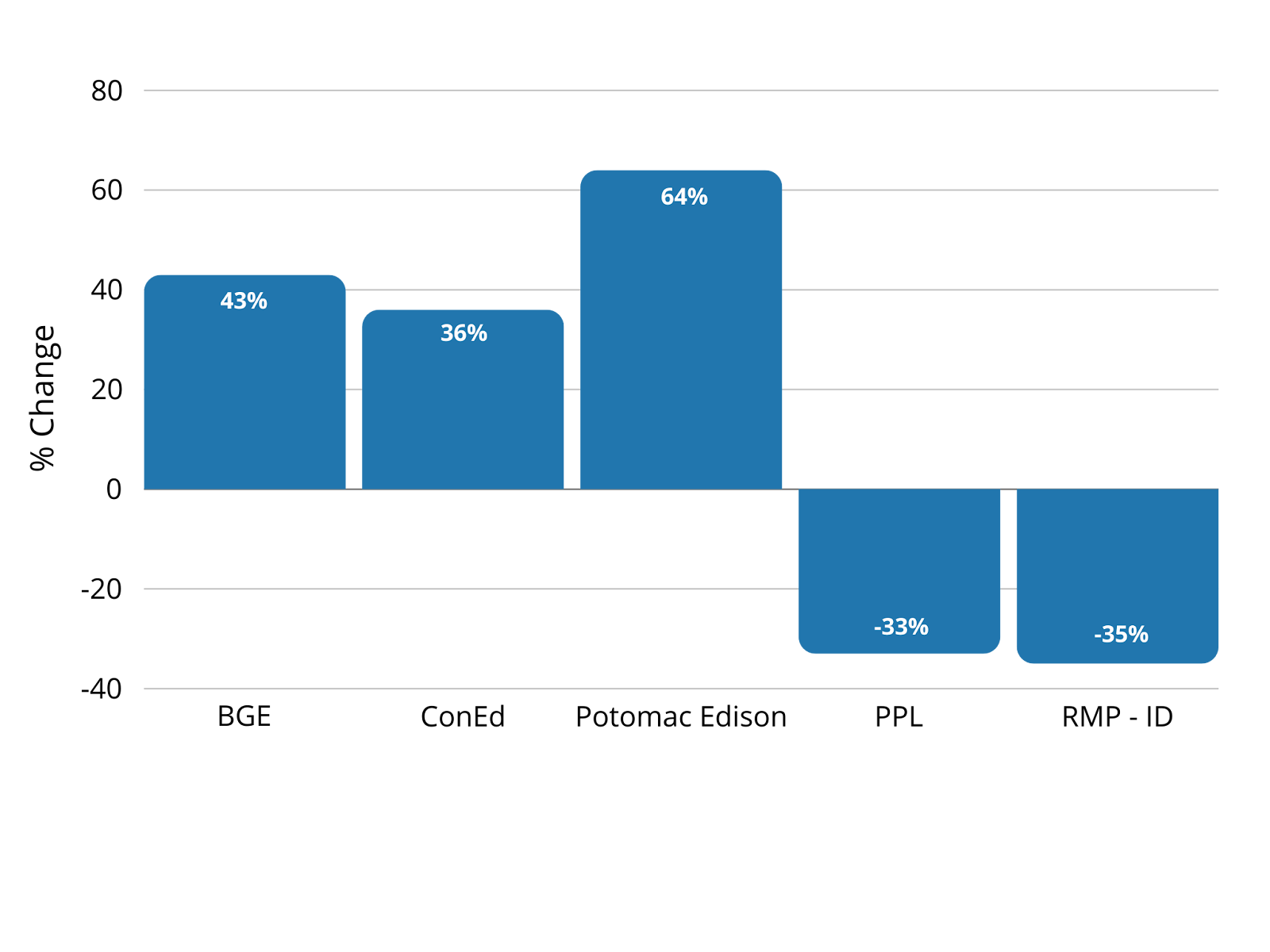

Individual program changes, from left to right: Baltimore Gas & Electric, ConEd, Potomac Edison, PPL, RMP (ID)

We’re already seeing a more lucrative midstream program in ConEd prior to the sunsetting of their downstream program, with rates already up 36% and a 25% bonus on fixtures. Two additional programs in Maryland, Potomac Edison and Baltimore Gas and Electric, saw substantial increases in their midstream programs, up 64% and 43% respectively. Of the handful of states that saw overall decreases in midstream rates, two can be attributed to large swings in single programs: PPL in Pennsylvania and RMP in Idaho.

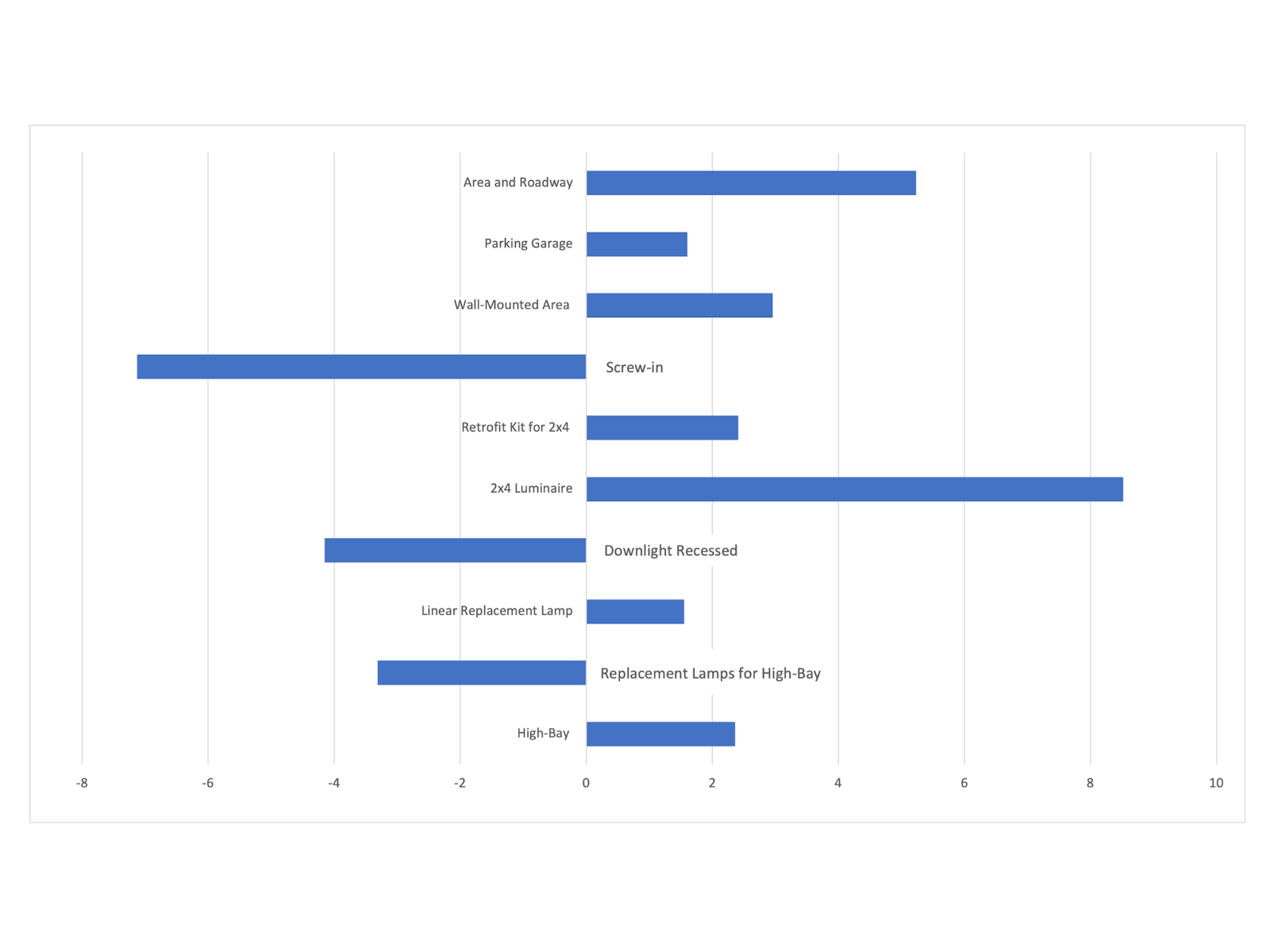

Midstream program percent changes by product category.

Many of the trends from downstream programs have logical counterparts in midstream programs. For example, while screw-ins have been surprisingly resilient in downstream programs, they’ve seen a sharp decrease across midstream programs. Fixtures are experiencing the largest increases, which mirrors the trend in downstream programs and suggests what programs are universally prioritizing in their new guidelines.

Fluorescent Bans

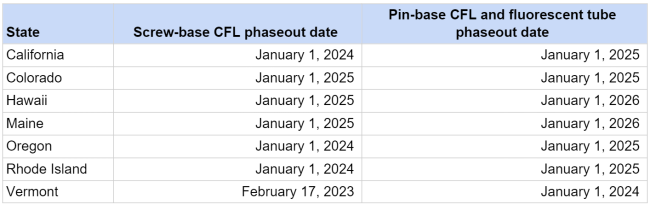

As we’re discussing lighting, it’s important to call attention to fluorescent bans that some states have begun rolling out. Vermont’s phaseout date is the first of a few states sunsetting these products, with their deadline passing at the beginning of 2024. In the pipeline before 2025 are California, Colorado, Hawaii, Rhode Island, and Oregon, with Maine coming in about a year later. As of now, it’s unclear if this trend will spread to other states or if this will impact HIDs at all. However, it’s certainly something to be mindful of, particularly for those who frequently work in the states that have already committed to phasing out these fixtures.

Update 3/11/24: Washington has since announced their prospective fluorescent ban for 2029. Read more about it here.

HVAC Program Trends

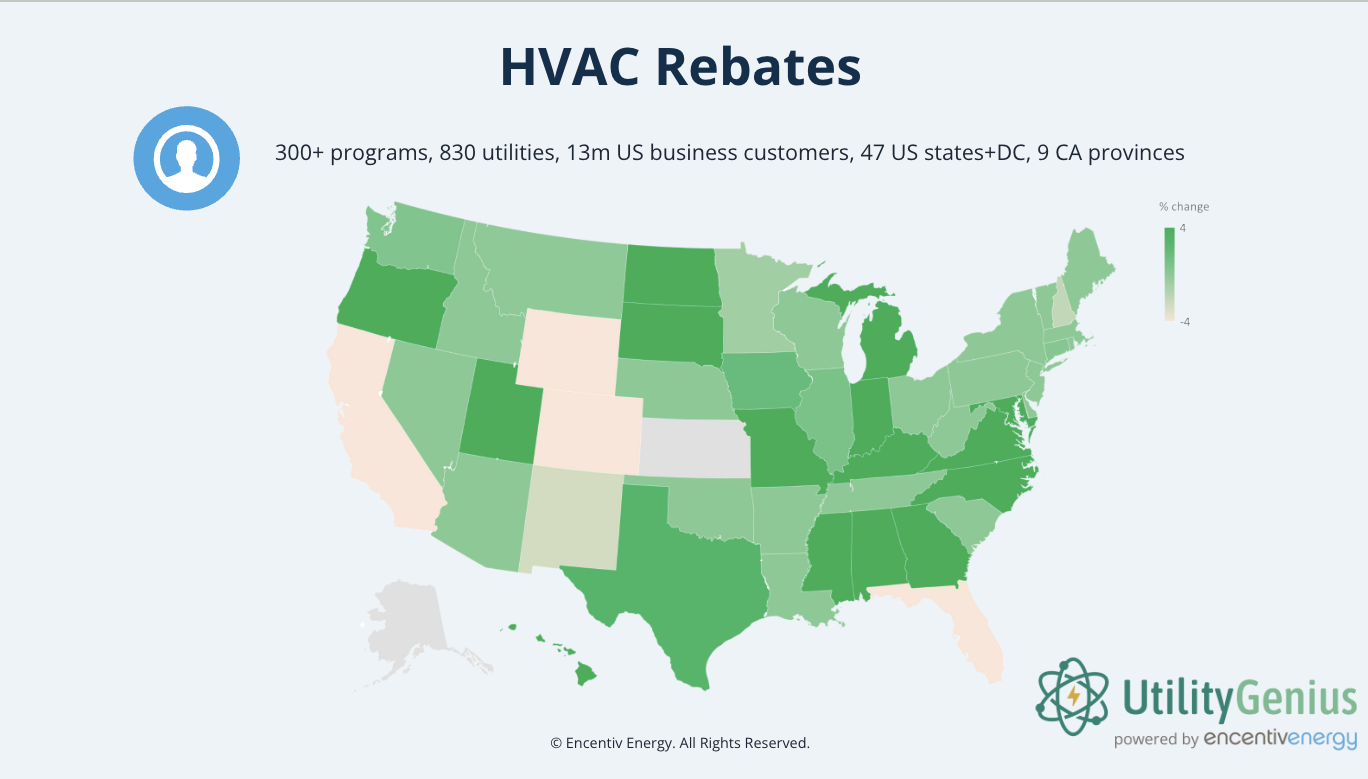

National HVAC rebate program overview.

Deviating from lighting for a second, let’s review some of the HVAC trends we’ve been seeing so far in 2024. As you can see in the map above, HVAC programs are broadly increasing, with a general 7% rise in rates across the programs in this analysis. HVAC program availability is also expanding, with six new programs being created this year. Existing programs are expanding as well, both to introduce midstream and incentivize more products, with heat pumps being the most popular.

Speaking of heat pumps, many programs have significantly increased their rates for these products, as well. In RMP/Utah, rates increased 25-75% for heat pumps only. In Quebec, heat pump rates were increased a whopping 300%. Something to keep an eye on in these programs is the separation of cold climate heat pumps.

Networked Lighting Controls and Horticultural Lighting

While we’ve covered broad lighting trends, there are two particular areas of focus within lighting to draw attention to. Horticultural lighting is a subset of lighting products used in various horticultural settings, primarily grow lighting. Networked lighting controls can improve the efficiency of your fixtures by giving you more control over conditions, such as when lights are on or the brightness of them.

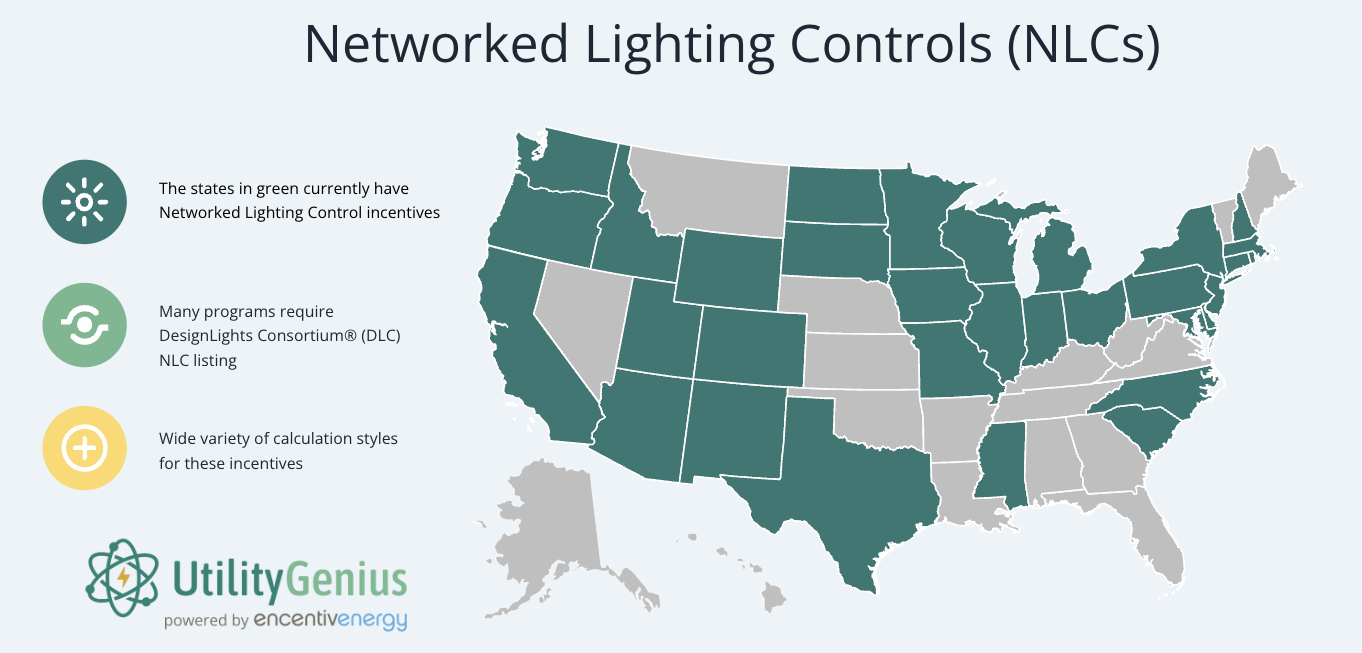

Networked Lighting Controls

NLC rebate availability has stayed relatively stable this year. States introducing new NLC programs for 2024 include Ohio, New Hampshire, Connecticut, and Mississippi. Calculations for NLC incentives vary widely between programs, though one similarity many have is the DLC listing requirement for these products. Be sure to check programs in your state for specifics on completing a qualifying NLC installation.

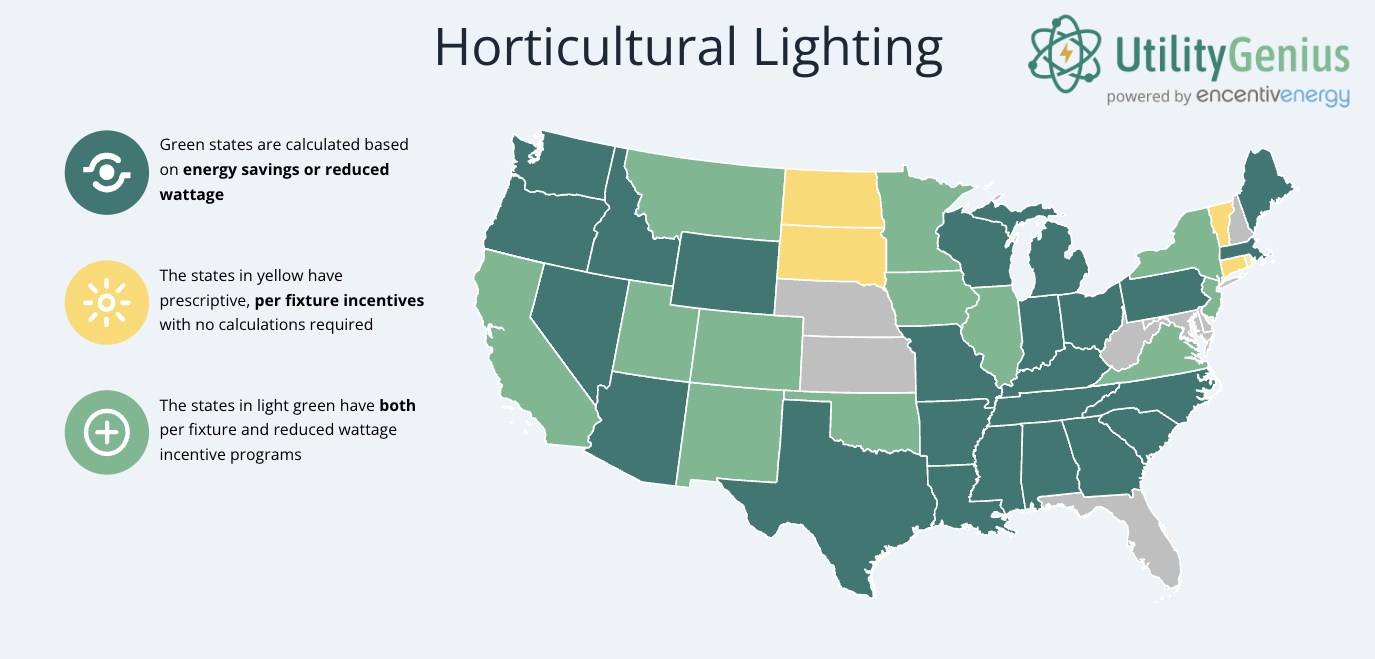

Horticultural Lighting

The horticultural lighting picture for the U.S. looks very healthy going into 2024, with some important changes for eligible equipment dropping soon. While coverage is still widely available, one important change from 2023 is the shift towards rebates calculated based on energy savings vs. per fixture. While some states are incentivizing both per fixture and energy savings, states that only offer per fixture incentives are shrinking.

The energy savings calculations for horticultural lighting are distinct from other energy savings calculations, so here’s a brief breakdown of two common ways these incentives might be calculated. The first is Photosynthetic Photon Efficacy (PPE), which measures a grow light's efficiency at converting electricity into PAR light (the spectrum of light used by plants for photosynthesis). Programs like ComEd in Illinois base their program calculations on PPE improvement per watt, with a minimum requirement of PPE. The second type is Photosynthetic Photon Flux (PPF), which measures the total amount of PAR produced by a light in a given second. Arizona Public Service’s program calculates its incentive based on total PPF at different stages of the growth cycle.

There are additional ways that horticultural lighting rebates can be calculated, but if you come across these terms in programs, bookmark these definitions so you can be prepared.

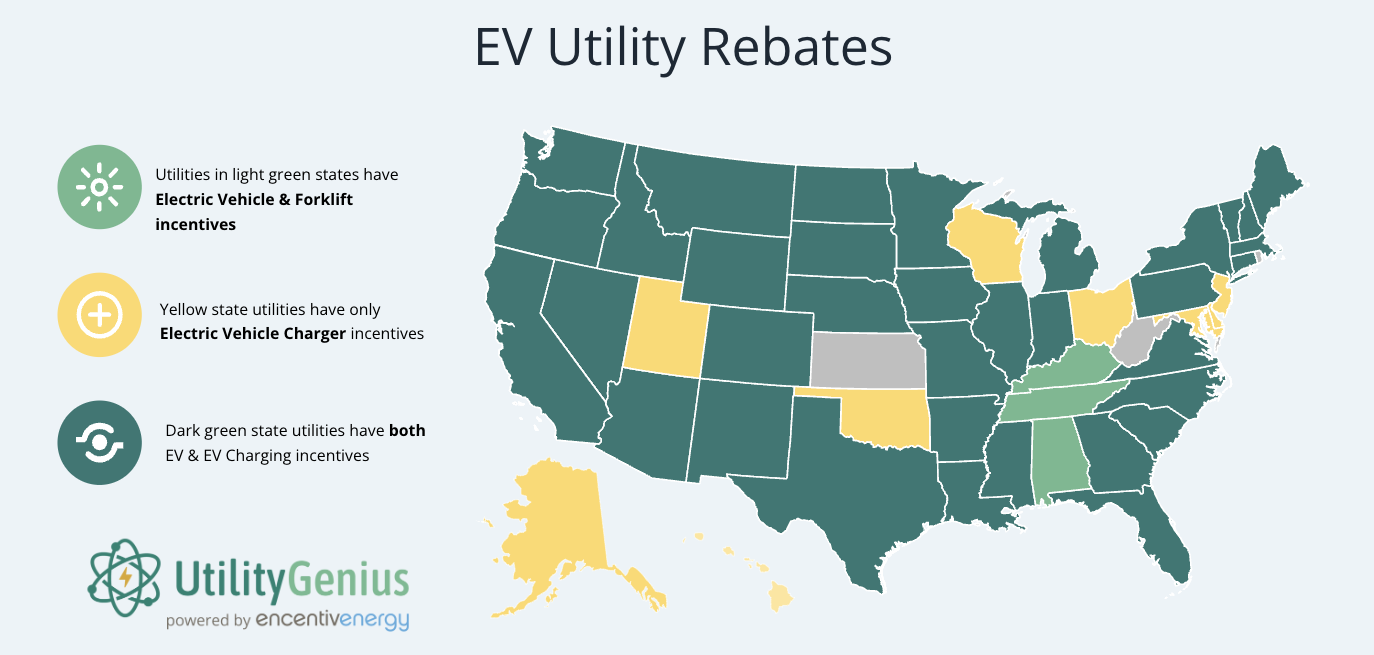

Electric Vehicles and Chargers

Similar to our takeaway in 2023, the EV program saturation has maintained into 2024, with nearly every state having programs available for either vehicles and charging, with a vast majority of states incentivizing both. Many programs have shifted from solely incentivizing chargers to including vehicles in their program, showing an interest in fleet electrification. The wide availability of charging incentives supports necessary infrastructure improvements to shift towards electric vehicles, as well. Overall, the saturation of EV incentives will alleviate range anxiety for those still on the fence about making the change, and we expect to see this trend continue.

Key Takeaways

There’s a lot of rebate information to sort through at the beginning of every year; we’re here to help. Below is a short summary of our key takeaways to keep in mind in 2024:

- Lighting rebates remain strong! There’s an increase in midstream program availability, with some major programs going midstream only this year. Prescriptive incentives are also available as these programs rebound from EISA.

- Keep an eye on potential fluorescent bans across the country. While only some states are currently eyeing deadlines for these products, more could follow.

- HVAC programs remain strong, with many programs emphasizing heat pumps in particular.

Whether you’re a distributor, a manufacturer, or a contractor, we have more solutions to help you utilize rebates in 2024. Reach out to us at hello@encentivenergy.com with questions!